Does the price you pay

for shares actually matter?

The short answer: yes – more than almost anything else.

When it comes to the Australian share market (the ASX), the price you pay today has a huge impact on the returns you get tomorrow. Not just a little – a lot.

There’s a measure called the PE ratio (Price-to-Earnings ratio) that tells you exactly how expensive the market is at any given moment. And once you understand it, you start to see the share market very differently.

What is the PE ratio?

Think of it like this.

Imagine a business makes $1 in profit per year. If someone offers to sell you that business for $15, you’re paying 15 times its annual earnings – a PE of 15.

If they want $23 for it, that’s a PE of 23.

The lower the PE, the less you’re paying for each dollar of profit. The higher the PE, the more you’re paying. Simple enough. But here’s why it matters so much. To Learn more about the PE Ratio we have a guide here: Price to Earnings Ratio Formula and Examples

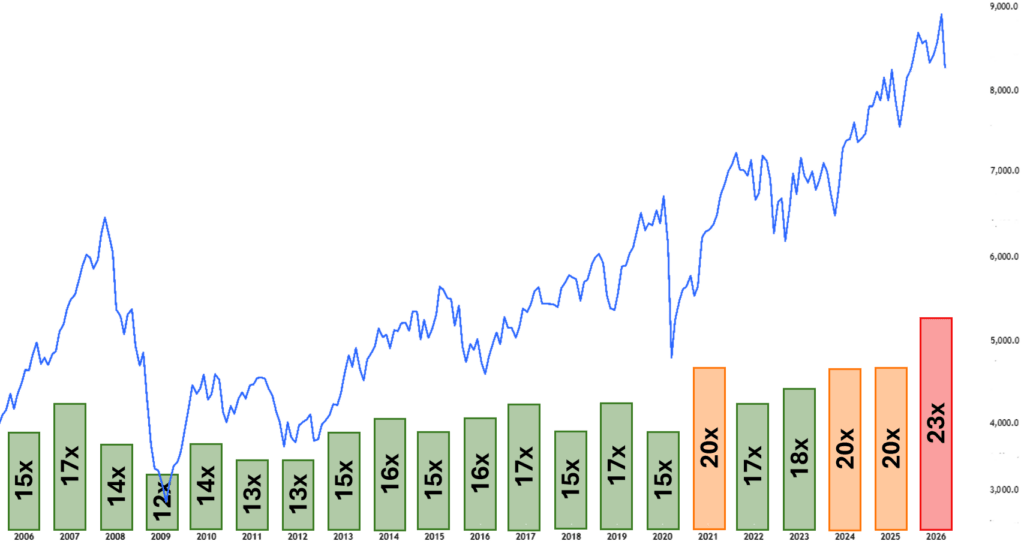

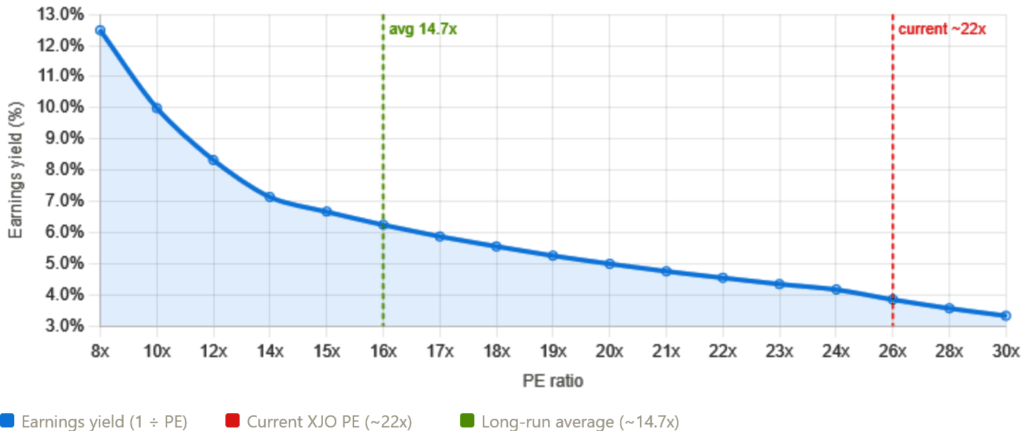

What does the ASX’s long-run average look like?

Over about 20 years, the ASX has averaged a PE of around 14.7 times earnings. Here’s a rough guide to what different PE levels have historically meant for long-run returns:

| PE level | What it means for you |

| Below 12× | Strong forward returns – rare and worth acting on |

| 12–15× | Solid returns – the sweet spot historically |

| 16–18× | Moderate, mixed – still reasonable |

| 19–20× | Returns start compressing – be more selective |

| 21–24× | Lower expected returns – discipline matters most |

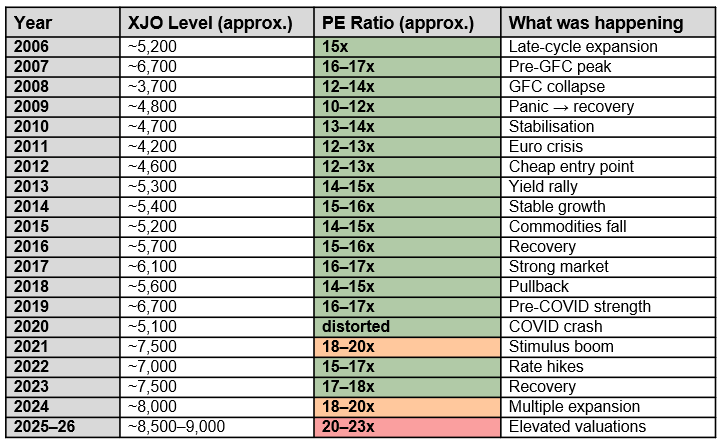

Right now (March 2026), the ASX is trading at roughly 22–23 times earnings on a trailing basis, or around 18–20 times on a forward estimate (based on expected earnings over the next 12 months). Either way – above the long-run average.

Why is the ASX different from the US market?

This is worth understanding, because the rules aren’t the same everywhere.

The US share market (the S&P 500) is full of big technology companies – Apple, Microsoft, Nvidia – that the market is willing to value at high multiples for long periods. They have sticky business models, high margins, and genuine long-term growth. High PEs can persist.

The ASX is built differently. Its biggest sectors are:

- Resources (BHP, Rio Tinto, Fortescue) – highly cyclical, earnings go up and down with commodity prices

- Banks (the Big Four) – sensitive to interest rates, credit cycles, and housing

Both sectors are known for paying big dividends rather than reinvesting earnings for growth. Both have earnings that boom and bust over time. The market knows this, so it prices them at lower multiples on average – and when PE gets too high, it tends to snap back hard.

That’s why the PE-to-returns relationship is especially powerful on the ASX. There are fewer companies that can sustain high valuations here than in the US.

The three zones explained

Green zone – PE 15 to 18× – build your position

This is the sweet spot for ASX investors. You’re not overpaying, earnings are doing most of the heavy lifting, and you have the potential for valuation expansion on top of that.

What works here:

- Steadily accumulating quality companies – banks, healthcare, industrials

- Dividend plus growth combinations (the ASX pays some of the best dividends in the world)

- Staying invested and letting compounding do its job

Expected long-run return: roughly 7–10% per year, plus dividends on top of that. Low risk of the valuation being pulled out from under you.

Yellow zone – PE 19 to 20× – be selective

The market has gotten more expensive. It’s now pricing in optimism – meaning companies need to deliver on high earnings expectations, or the market re-rates them down.

Index buying becomes less attractive here. The whole-market return probably compresses to 4–8% per year. But you can still do well if you’re picking carefully.

What works here:

- Focusing on companies with genuine earnings upgrade stories – businesses that are likely to beat expectations

- Looking for sectors that haven’t run up as much (resources during a down cycle, for example)

- Being willing to hold cash and wait for better entry points

Red zone – PE 21 to 24× – play defence

This is where the ASX is right now.

The market has already re-rated higher – the gains from investors simply being willing to pay more for each dollar of earnings have already happened. From here, the only engine left is earnings growth, and there’s real risk of the valuation compressing back toward average.

Expected long-run returns: roughly 0–5% per year. Not zero risk of a correction, either.

What works here:

- Trimming positions that are fully valued and rebalancing

- Keeping some cash ready – volatility creates entry points, and it’s better to have dry powder than to be fully invested at stretched valuations

- Being very selective: M&A situations, genuine deep value, or structural growth stories with clear earnings catalysts

This doesn’t mean panic. It means discipline.

The moments that created real wealth

If you zoom out across the last 20+ years on the ASX, two entry points stand out above everything else.

2003 – coming out of the dot-com bust, earnings depressed, sentiment cautious. PE was low. Both return engines were primed.

2009 – the Global Financial Crisis. The market had fallen almost in half. Bank earnings had been smashed. Resources were soft. It felt genuinely frightening. PE: around 14–15× deeply depressed earnings.

Both of those moments felt dangerous at the time. Both turned out to be among the best wealth-creation opportunities of a generation.

That’s the uncomfortable truth about investing by valuation. The best opportunities almost never feel like opportunities when you’re standing in them.

The thing most people get backwards

High PE periods tend to feel safe. Prices are rising, the news is good, everyone around you is making money. It’s easy to stay invested or even add more.

Low PE periods tend to feel risky. Something has usually gone wrong – a financial crisis, a commodity bust, a recession. It’s psychologically hard to act.

But the evidence is clear. The biggest mistakes get made at high PEs, not low ones. Buying when everything feels safe but is actually expensive is how long-term returns get destroyed.

What does this mean for you right now?

At a PE of 22–23×, the ASX is pricing in an optimistic scenario. That doesn’t mean a crash is coming. But it does mean:

- The margin of safety is thinner than it was five years ago

- Prospective returns from here are lower than historical averages

- The companies you own and the prices you pay matter more than usual

- Keeping some capacity to act when markets pull back is valuable

You don’t need to predict what the market will do. You just need to adjust your behaviour to match the environment.

Low PE? Build.

Medium PE? Be steady.

High PE? Be disciplined.

The market will give you another good entry point eventually. It always does.

What you learn here has been used in our Trade for Good software.

Click on the button to find our software education videos.

You can read more of our educational articles in the Trade for Good Learn section

Trade for Good Learn